The boom pulled a decade of production forward. What comes next is not a crash — it is a repricing, and it favors whoever can find the inventory a home.

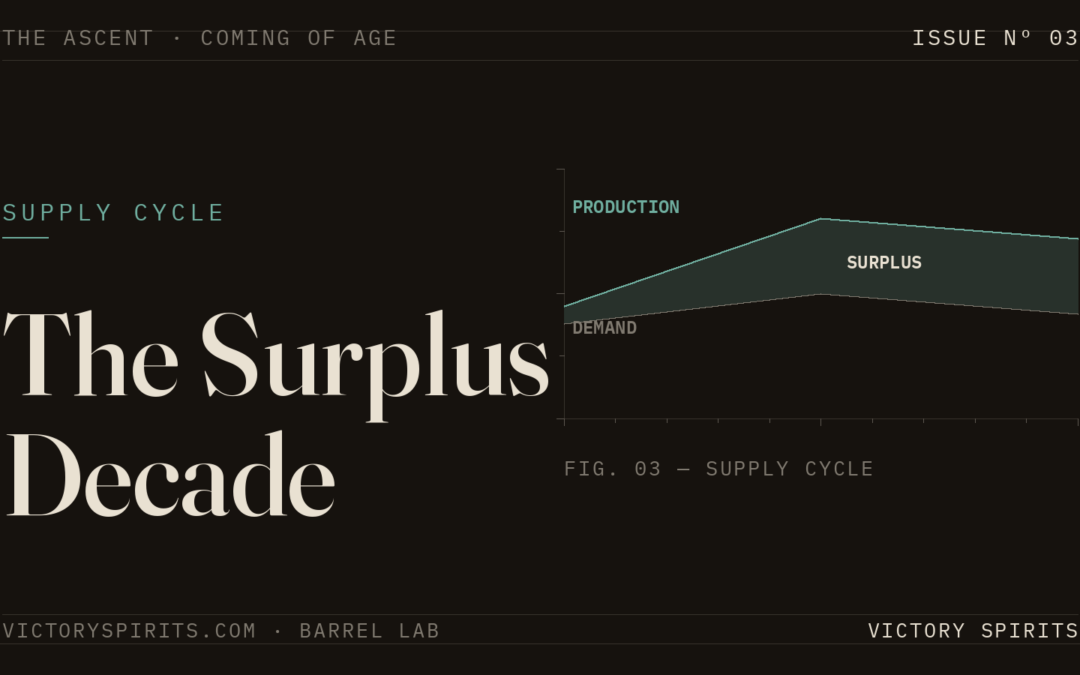

Booms end the same way. Demand climbs, everyone lays down more than they can sell, and the barrels keep aging on a schedule that does not care what the market did last quarter. The bourbon boom pulled years of production forward against a demand curve that assumed the line only went up. The line did not only go up. What sits in warehouses now is the result: real surplus, aging on its own clock, held by producers who would rather move it than carry it another season.

The reflex is to call this a glut and treat it as a threat. That reads the situation exactly backwards. A surplus is not a crisis for the people who buy — it is the best sourcing environment in a generation. The threat is only real for those who cannot solve the problem a surplus actually creates, which is not oversupply. It is discovery.

What “surplus” actually means

Whiskey is a strange commodity because production and demand are separated by years. A distillery deciding how much to lay down in 2020 was betting on 2024, 2026, 2028. Those bets were placed at the top of a boom, by producers expanding capacity, by contract distillers filling every rickhouse they could build, by new brands sourcing aggressively because barrels were scarce and getting scarcer. Every one of those decisions was rational in isolation. In aggregate they produced more aging inventory than the near-term market can absorb at boom prices.

Tracking the clearing price for a 10 year old barrel of bourbon over the decade. (source: Victory Spirits Development, excerpt of analysis to be released at the American Distilling Institute conference in Miami, August 19, 2026)

hat inventory does not disappear. It ages. It accrues carrying cost. It ties up capital and warehouse space that a producer would rather deploy elsewhere. And at some point the barrel that was laid down as an appreciating asset becomes an obligation — something that has to find a buyer, because the alternative is holding it indefinitely against a market that has already moved on. Multiply that across hundreds of distilled spirits plants and you have the defining condition of the next several years. Not scarcity. Abundance, scattered and looking for a home.

Why this is a repricing, not a collapse

The word “crash” implies value evaporating. That is not what a whiskey surplus does. The spirit is still real, still aging, still worth something to someone building a brand. What changes is the price, and the direction of leverage.

In a scarcity market the seller sets terms. Barrels are hard to get, buyers compete, and the producer names a number that holds because the next buyer is right behind the last one. In a surplus market that dynamic inverts. The barrels are available, the buyers are fewer relative to the inventory, and the producer’s leverage shifts from “name your price” to “find your buyer.” Prices soften — not to zero, but toward a level where the spirit actually clears. For a brand owner, a blender, or an NDP with capital and patience, this is the environment you wait a decade for. Quality inventory, at a basis that finally makes sense, with the leverage on your side of the table.

The surplus does not destroy value. It redistributes it — from the people who overproduced to the people positioned to source well. The only question is whether the market can connect the two efficiently. That is where the old model breaks.

The constraint moved, and the phone call didn’t

When barrels were scarce, relationships were sufficient. You only had to know the few people who had what you needed, and the whole game was access. Now access is trivial — the inventory is everywhere. The binding constraint has moved downstream, from who has it to how do the right barrels find the right buyer at a price both can trust. That is a matching problem, and matching at scale is precisely what a network of phone calls cannot do.

Consider what the old model does to a surplus. A producer with inventory to move calls the buyers he knows. Those buyers may not need it, or may lowball because they can sense distress, or may simply not be the right home for that particular spirit. Barrels that should have cleared sit stranded, not because there was no buyer in the market but because the buyer and the seller never found each other. Meanwhile the prices that do get struck happen in private, so the next producer has no reference for what his inventory is worth and either holds too long or sells too cheap. The surplus makes every weakness of the opaque market worse: more inventory to match, less shared information to match it with, and more value lost in the gap.

The surplus rewards legibility

A transparent market does for a surplus exactly what it does for a scarcity — it makes value visible to both sides — but the stakes are higher when inventory is abundant, because the cost of not matching is inventory that never clears at all.

For the seller, a marketplace turns a warehouse full of obligations into structured listings in front of every qualified buyer at once, priced against a reference the buyer can trust, which is the difference between moving inventory and dumping it. For the buyer, it turns a scattered, opaque field into something searchable, comparable, and checkable — the ability to source the right barrels at a defensible basis instead of taking whatever a broker happens to surface. The surplus is a buyer’s market only if the buyer can actually find what the market holds. Legibility is what makes that possible.

This is the decade the reference layer was built for. The inventory is here, the leverage has shifted, and the market that connects supply to demand efficiently will capture the value that the phone-call market strands. The surplus is not the problem. Opacity is. And the two do not survive together for long.

The Ascent — Coming of Age. A bi-weekly series on the structure and future of the bulk whiskey market, from the team building Victory Spirits Barrel Lab.